- Daly Asset Management

- Posts

- The Gap Between Euphoria and Reality Is Widening

The Gap Between Euphoria and Reality Is Widening

What the Nasdaq's winning streak isn't telling you.

Liam Daly

April 17, 2026

Corporate Overview

The Nasdaq’s 12-session winning streak has pushed markets into a state of unearned euphoria that ignores crumbling macro foundations. While the consensus bets on a swift geopolitical resolution, reality shows a sharp deceleration in consumer spending and a closed Strait of Hormuz choking global supply chains.

With the Atlanta Fed slashing GDP growth estimates to 1.3% and inflation projected to hit 3.6%, the "pivot" narrative is dead. Daly Asset Management provides the systematic, independent research needed to navigate this transition from momentum to macro reality.

Start Your Investment Profile → app.dalyassetmanagement.com/signup

Daly Asset Management is built around one principle: independent thinking, data-driven allocations, and zero tolerance for high-fee mediocrity. We're systematic, transparent, and we don't bet the farm on hope.

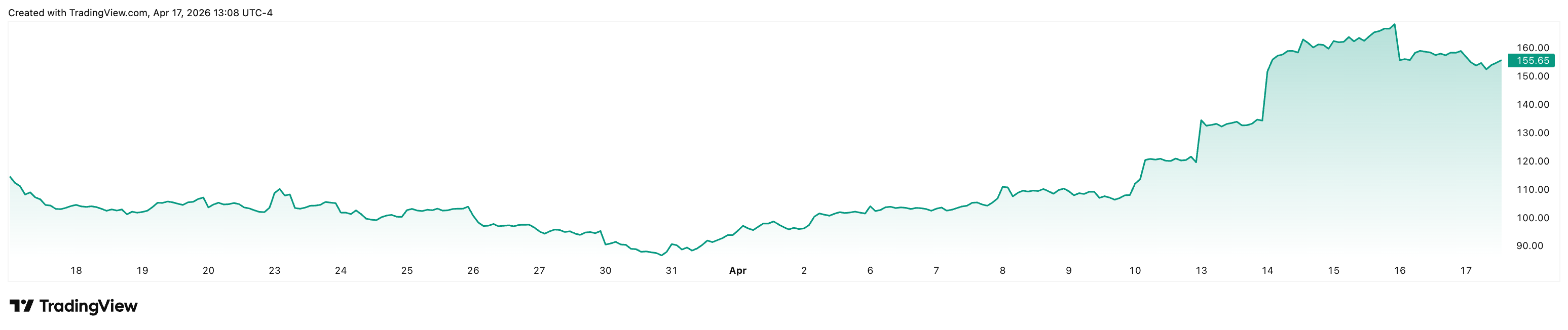

Stock of the Week

Ticker: CRDO | Sector: Technology | Market Cap: $29.3B | Yield: N/A

Why Now:

As of April 17, 2026, Credo is transitioning from a niche cabling provider to a full-stack optical connectivity powerhouse. The stock has surged 65% since February, fueled by strong data center spending and the strategic acquisition of DustPhotonics for approximately $1.3 billion. This move integrates silicon photonics into CRDO’s portfolio, positioning them to lead the 1.6T and 3.2T cycles. Despite the rally, CRDO trades at a PEG ratio of 0.62, a significant discount to networking peers like Marvell and Broadcom, suggesting the market is still underpricing its long-term growth trajectory in optical transceivers.

Risks:

The primary risk is the eventual "copper wall"—if the industry shifts to optical faster than CRDO can scale its transceiver production, margins could compress during the transition. Additionally, customer concentration remains high, as a pivot by a single hyperscaler like Amazon could materially impact quarterly revenue.

Verdict:

A "Strong Buy" for aggressive growth portfolios looking to capitalize on the next phase of AI infrastructure.

Market Snapshot

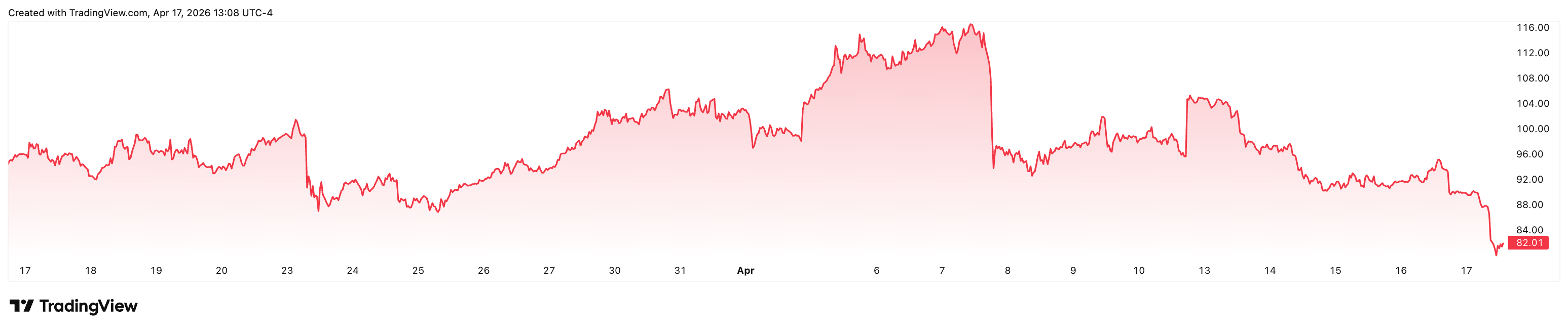

The week ending April 17, 2026, was defined by a sharp "de-risking" event as geopolitical tensions in the Middle East and a hot CPI print forced a repricing of the terminal rate.

Asset | Close (17 April 2026) | Weekly Change (%) |

S&P 500 | 7,109.97 | +4.30% |

Nasdaq Composite | 24,457.36 | +5.31% |

Dow Jones Industrial Average | 49,598.58 | +3.51% |

Russell 2000 | 2,772.75 | +5.40% |

10Y Yield | 4.25% | -5.56% |

Crude (WTI) | $81.28 | -13.91% |

Gold | $4,804.38 | +1.08% |

Bitcoin | $75,905.00 | +3.29% |

The week signifies a massive "risk-on" rally fueled by cooling geopolitical tensions and a sharp drop in energy costs. The simultaneous surge in equities and plunge in oil/yields suggests investors are pricing in lower inflation and a more accommodative Federal Reserve. Overall, the market transitioned from fear-based hedging to aggressive growth positioning as systemic risks eased.

Market Commentary

Hormuz Reopening Triggers Bullish Surge

Wall Street hit record highs Friday as Iran declared the Strait of Hormuz "completely open" for commercial vessels following the Israel-Lebanon ceasefire. Markets rallied on the de-escalation: the S&P 500 rose 1% while the Dow jumped 1.9%. Crude prices collapsed to $83 as the supply risk premium evaporated, and the 10-year Treasury yield slid to 4.24%.

However, the relief remains fragile. President Trump maintained that the U.S. naval blockade on Iranian ports stays "in full effect." Economists warn that the "litmus test" is whether shipping operators actually return, which is required to restore global energy flows.

Wholesale Prices Defy War Shock

March Producer Price Index (PPI) data arrived as a rare cooling signal amid geopolitical heat. Wholesale prices rose 0.5% monthly, significantly trailing the 1.1% consensus estimate. More striking was core PPI, which stripped out volatile food and energy to land at a meager 0.1%.

While gasoline surged 15.7% due to the conflict, flat services costs suggest the underlying inflationary pulse remains muted. However, the annual headline rate hit 4%, a three year high. This divergence keeps the Fed "firmly on hold" as businesses begin absorbing tariff and energy costs rather than passing them to consumers.

Nikkei Record as Geopolitics Ease

Japan’s Nikkei 225 surged 2.38% to a record 59,518.34 this week, riding a wave of optimism over a potential U.S. and Iran peace deal. While the S&P 500 reclaimed its pre-war losses, the rally was truly global; South Korea’s Kospi jumped 2.21% and China’s GDP beat expectations at 5% growth.

This "peace dividend" is currently outweighing the energy shock, with markets pricing in a diplomatic resolution. However, it’s best to remain cautious. Until a deal is signed, this is a headline-driven rally susceptible to sudden reversals if negotiations stall or White House rhetoric shifts.

War Volatility Boosts Bank Profits

Wall Street’s giants are thriving on the chaos. The big six lenders reported a combined $47.4 billion in Q1 profits as the US-Israeli conflict with Iran sent trading desks into overdrive. While investors fled to safe havens, JPMorgan reported a 13% profit jump and Goldman Sachs surged 19%.

This isn't a sign of economic health; it's a reflection of panic-driven turnover. Banks are aggressively returning this windfall to shareholders, with JPMorgan hitting a record $8.3 billion in buybacks. High earnings today mask the growing risk of a war-induced global recession.

Tactical Map

Tactical De-risking: After a parabolic equity rally to new all-time highs, following the opening of the Hormuz Strait, extreme overbought conditions (RSI near 86) and record-low consumer sentiment suggest a pivot toward defensive positioning and capital preservation.

Capitalizing on Institutional Volatility: Large-cap banks are extracting record profits from trading turnover; we view their aggressive buybacks as a tactical yield play amidst broader recessionary risks.

AI Hardware as a Margin of Safety: With semiconductor earnings projected to grow 80%, we maintain an overweight position in IT and Emerging Markets at their lowest valuations since 2020.

Theme to Watch

One noticeable trend currently playing out is the outflow of capital from the GCC toward Singapore and Hong Kong as a strategic geopolitical hedge. While the "capital shift" isn't a wholesale exodus, entities like Saudi Arabia’s Public Investment Fund (PIF) have aggressively scaled Asian allocations in recent years, with PIF alone committing $6.6 billion to the region.

This multi-directional flow sees Gulf funds seeking entry into mainland China via Hong Kong, while Asian family offices simultaneously relocate to Dubai to escape tightening Singaporean regulations. For investors, this "Dual Hub Strategy" highlights a permanent move away from Western-centric portfolios toward a more resilient, pan-Asian/Middle Eastern axis.

Forward View

Monday, April 20: PBOC Interest Rate Decision (Late Sunday/Early Monday ET)

Wednesday, April 22: UK Consumer Price Index (2:00 AM ET) & Canada Consumer Price Index (8:30 AM ET)

Thursday, April 23: Japan Consumer Price Index (7:30 PM ET)

The focus shifts to global divergence as central banks face unique domestic pressures. Watch the PBOC for surprise stimulus and the UK/Canada CPI prints for evidence of "sticky" services inflation that could postpone rate relief.

In Japan, any print north of 2% increases the probability of a BoJ policy normalization, a move that would spark significant volatility in the Yen and carry trade unwinds.

Final Words

The era of unearned euphoria is hitting a wall of macro reality as global supply chains remain at the mercy of geopolitical headlines. The gap between headline euphoria and macro reality is widening, leaving unhedged investors vulnerable to the next reversal. Daly Asset Management bridges this gap by providing investors with the systematic, institutional-grade research required to outpace the consensus.

Click to Sign Up → app.dalyassetmanagement.com/signup

Disclosures: This newsletter is for informational purposes only and does not constitute investment advice. Past performance is not indicative of future results. Always conduct your own due diligence or consult with a financial advisor before making investment decisions.