- Daly Asset Management

- Posts

- The Fed Blinks, But Rotation Roars

The Fed Blinks, But Rotation Roars

Markets hit records as tech crumbles and the Fed signals one lonely cut for 2026. The real story? Capital is fleeing concentration risk.

Liam Daly

December 12, 2025

Daly AM Is Now Trading on Surmount

You can now invest directly in our three systematic strategies:

Daly Asset Management Core Income – Yield-focused, volatility-managed

Daly Asset Management Top Ten – Concentrated conviction plays

Daly Asset Management Core Return Focus – Total return optimization

Link your existing brokerage or deposit directly. These strategies execute automatically—no panic selling, no emotional overrides, no phone calls from someone who wants to "check in" during a drawdown. Just disciplined, rules-based allocation doing what it's supposed to do.

🧠 Corporate Overview

The market delivered a lesson this week that most on Wall Street will conveniently forget by Monday: concentration kills.

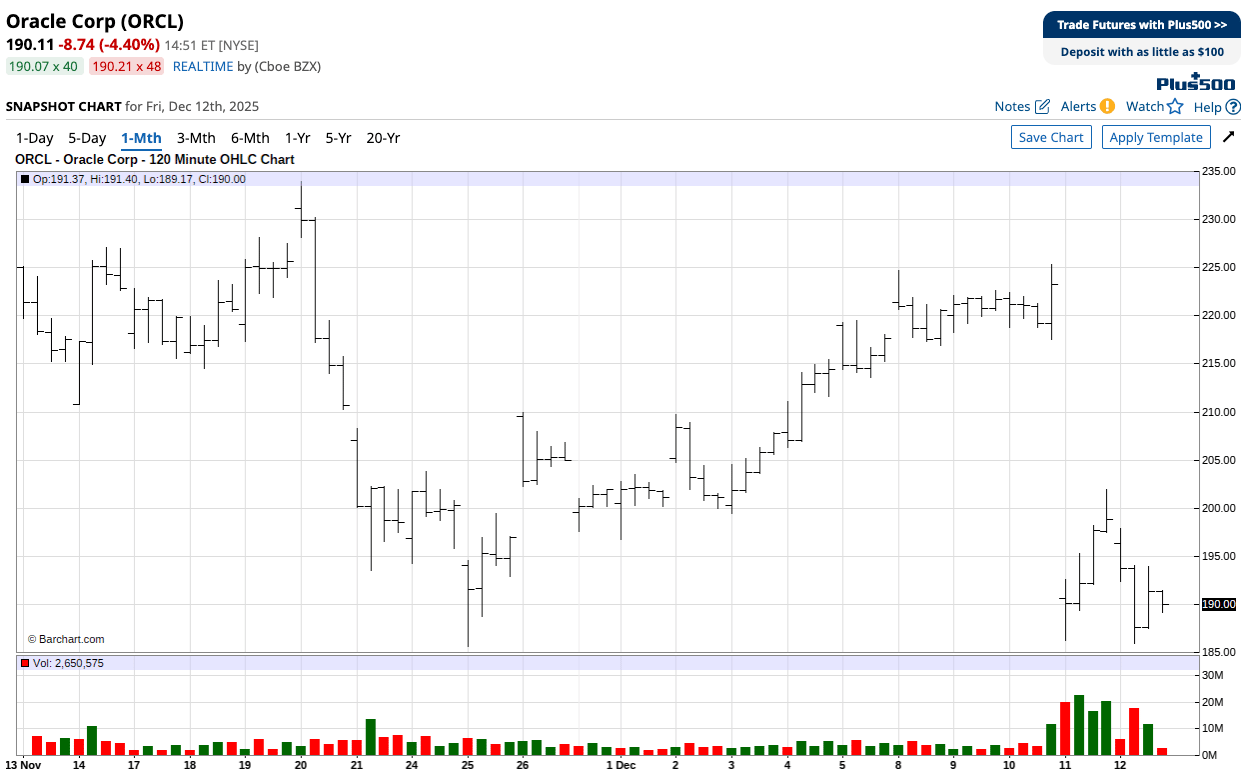

While the S&P 500 notched record highs and the Dow surged nearly 2%, the Nasdaq fell 1%—a divergence that hasn't mattered this much since early 2022. Oracle and Broadcom both beat earnings and promptly got demolished, shedding over 10% as investors finally asked the right question: What happens when AI capex doesn't deliver?

The Federal Reserve cut rates Wednesday for the third consecutive time, bringing the fed funds rate to 3.5%-3.75%. But Chair Jerome Powell's message was clear: we're done here. The updated dot plot projects just one measly cut in 2026, with three dissenters signaling a deeply divided FOMC. Powell blamed tariffs for inflation overshooting 2%, but wouldn't commit to anything beyond "we're well positioned to wait."

Translation: The easy money era just ended—even though most investors haven't realized it yet.

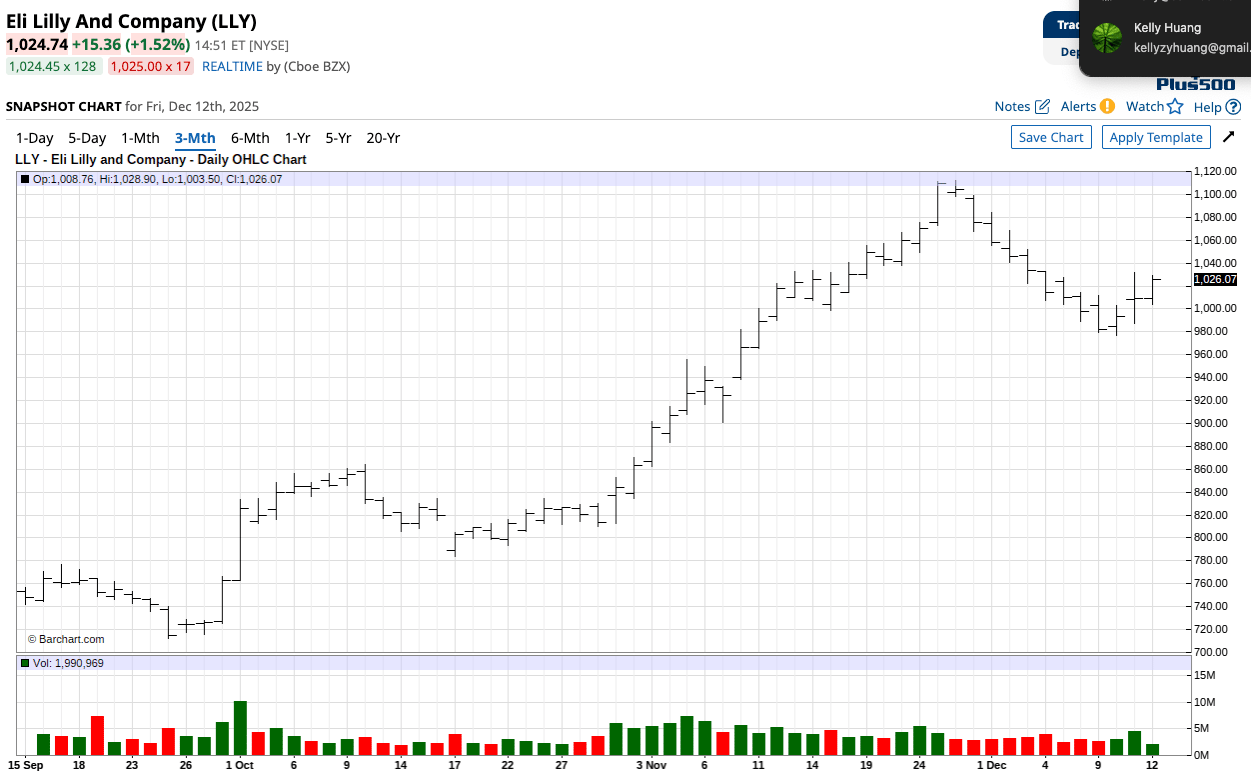

💡 Stock of the Week: Eli Lilly (LLY)

Ticker: LLY | Sector: Healthcare / Pharmaceuticals | Market Cap: ~$810B | Dividend Yield: 0.7%

Eli Lilly surged 4% Thursday after announcing its next-generation obesity drug delivered a staggering 23.7% average weight loss in late-stage trials while reducing knee arthritis pain. For context, the highest dose achieved 28.7% weight loss when excluding trial dropouts—numbers that would make this the most effective obesity treatment ever commercialized.

This week's sector rotation handed healthcare a spotlight it hasn't seen in months. The sector gained over 1% while tech bled, and Lilly's pipeline timing couldn't be better. With GLP-1 agonists becoming structural growth drivers—not fads—Lilly sits at the intersection of demographic tailwinds (aging populations, metabolic disease epidemics) and genuine innovation. The company's diversified portfolio beyond weight loss (oncology, immunology) provides downside protection that pure-play biotech can't match.

Macro-wise, this is textbook defensive growth. As the Fed signals restrictive policy and tariffs cloud GDP forecasts, pharma benefits from inelastic demand and pricing power. Lilly's international exposure (~45% of revenue) also hedges dollar strength while Trump's tariff regime creates supply chain havoc for goods-heavy sectors.

Risks to Watch

Regulatory risk remains—FDA approvals can surprise. Competitive pressure from Novo Nordisk's pipeline means Lilly can't rest. And if you believe the "Magnificent Seven will never die" thesis, you might see this week's rotation as temporary noise rather than a sustainable reallocation.

Verdict

We're constructive. Lilly combines genuine innovation, structural demand, defensive characteristics, and entry timing that benefits from tech's valuation compression. It's not a momentum trade—it's an allocation into quality at a moment when quality just started mattering again.

📉 Market Snapshot (Week of December 1-5, 2025)

Index | Close | Weekly Change | YTD |

|---|---|---|---|

S&P 500 | 6,870 | +0.5% | +17.8% |

Nasdaq Composite | 23,578 | -1.0% | +22.1% |

Dow Jones | 47,955 | +1.6% | +12.7% |

Russell 2000 | 2,591 | +1.2% | +13.1% |

10Y Treasury Yield | +9 bps | +32 bps | |

WTI Crude Oil | -1.8% | -18.0% | |

Gold (spot) | +2.7% | +64.0% | |

Bitcoin | -1.2% | +99.0% |

The Dow outperformed by 250 basis points over Nasdaq this week—the widest divergence since March. Flows are rotating from growth-at-any-price into cyclicals, value, and quality. The 10-year yield climbed despite Fed cuts as markets price persistent inflation and reduced future easing. Gold hit new all-time highs near $4,381 in October and remains elevated, outperforming Bitcoin YTD—a clear signal that "store of value" debates have been decisively won by the yellow metal in 2025.

📊 Market Commentary

The Fed's Hawkish Cut and the Myth of Easy Money

Wednesday's 25bp cut was the least dovish rate reduction in modern memory. Powell all but admitted the Fed is approaching neutral—that mythical level where policy neither stimulates nor restricts. The updated dot plot showed a median forecast of one cut in 2026, but the distribution tells the real story: seven officials penciled in zero cuts.

This isn't consensus-building. It's a central bank admitting it has no idea what comes next.

The FOMC vote split 9-3, with Goolsbee and Schmid dissenting for no cut (too much inflation) while Governor Miran wanted a 50bp cut (too much labor weakness). It's the most divided Fed in six years. Powell acknowledged the November shutdown delayed critical data, but let's be honest: he's stalling. Core PCE remains at 2.8%—well above target—while unemployment hovers at 4.4%. The dual mandate is in tension, and Powell's solution is to do nothing and hope.

Markets aren't buying it. The 10-year yield rose 9 bps this week even as the Fed cut—a sign that term premium is back and inflation expectations remain sticky. Futures markets now price two cuts in 2026, defying the Fed's guidance entirely. Either the market thinks Powell's bluffing, or a recession's coming. Pick your poison.

AI's Reckoning: When Capex Becomes a Liability

Oracle cratered 10% Wednesday after missing revenue and announcing a $15B capex increase. Broadcom followed Thursday, losing 10% despite beating on every metric and guiding AI chip revenue to double in Q1. The problem? Margins are compressing as these companies front-load infrastructure spending without corresponding revenue visibility.

This is the moment skeptics have been waiting for. AI stocks priced in a world where capital never questions returns. Now it's questioning. AMD, Palantir, and Micron all sold off hard Friday as contagion spread. The Philadelphia Semiconductor Index dropped 5%—the worst day in two months.

Here's the uncomfortable truth: AI infrastructure is a CapEx sinkhole with unclear payback periods. Cloud providers are spending hundreds of billions building data centers that may not generate returns for years. Broadcom's $73B backlog over 18 months sounds great until you realize it's locking in razor-thin margins on custom chips. The AI trade isn't dead—but it's evolving from "growth at any cost" to "show me the cash flow." Most names won't survive that transition.

Trump's Tariff Regime: Chaos as Policy

Tariffs now cover 67% of U.S. goods imports—the highest since the 1930s. Trump's reciprocal framework has created a patchwork of rates ranging from 10% baseline to 50% on select partners. The economic impact is starting to show: Swiss GDP contracted sharply in Q3, Canada shed 36,500 manufacturing jobs, and Brazil's coffee exports to the U.S. collapsed under 50% duties.

Domestically, the picture's mixed. The U.S. trade deficit hit a five-year low in November as imports fell 5%. But that's not "winning"—it's demand destruction. Corporate America is frontloading inventory ahead of further escalations, creating a working capital squeeze that's straining balance sheets. Supply chains are fragmenting: China's exports to Vietnam, Indonesia, and India surged 20%+ as manufacturers reroute through third countries to avoid U.S. duties.

The Fed acknowledges tariffs are driving inflation, but Powell won't say it's a policy mistake—he can't. Trump's already threatened to replace him in May. This creates an impossible dynamic: fiscal policy is inflationary, monetary policy is restrictive, and both are politically toxic. Good luck threading that needle.

Gold's Moment: Store of Value Debate Settled

Gold surged past $4,340 this week, closing in on its October all-time high of $4,381. It's up 64% year-to-date—outperforming Bitcoin's 99% gain on a risk-adjusted basis and crushing equities. Silver hit $64.51, up 112% YTD, driven by industrial demand from solar, EVs, and AI infrastructure.

Bitcoin, meanwhile, traded flat near $92,000—down 28% from its October peak. The "digital gold" narrative is officially dead. When real rates rise and liquidity tightens, Bitcoin trades like a levered tech stock, not a safe haven. Precious metals are winning because central banks are buying (projected 900 tonnes in 2025) and retail investors are fleeing volatility.

This matters for asset allocation. If you're building a portfolio for uncertain times—tariffs, sticky inflation, geopolitical risk—gold and silver are proven hedges. Bitcoin is a speculation masquerading as insurance.

Rotation Isn't Noise—It's Signal

This week's market action was textbook: defensives and value outperformed, growth and momentum lagged. Financials, healthcare, and industrials led while tech hemorrhaged. The Russell 2000 gained 1.2%, outpacing the S&P by 70 bps. This isn't a one-week blip—it's the beginning of a broader deconcentration trade.

The Magnificent Seven's dominance is eroding. None of the top 25 S&P constituents by weight rank among 2025's best three performers. Breadth is improving, volatility is falling, and capital is rotating into overlooked pockets of the market. For systematic investors, this is alpha generation season. While passive indexers get whipsawed by tech concentration risk, active strategies can exploit dispersion.

🧭 Tactical Map: Where to Lean In

Healthcare Defensives: Pharma and med-tech benefit from inelastic demand, pricing power, and structural demographic tailwinds. Lilly, Merck, and Abbott look compelling.

Financials Rotation: Banks and insurers gain from higher-for-longer rates and steeper yield curves. Regional banks offer leveraged upside if the Fed pauses successfully.

Energy Contrarians: WTI at $57 is pricing in recession. If growth stabilizes, energy becomes the highest-beta value trade available.

Gold/Silver Exposure: Physical or ETFs—take your pick. Central banks aren't stopping, and geopolitical risk isn't fading.

Quality Over Growth: Look for companies with positive free cash flow, low leverage, and sustainable margins. The market's done rewarding promises—it wants proof.

🔍 Theme to Watch: The Great Deconcentration

For two years, the Magnificent Seven accounted for essentially all S&P 500 gains. That era is ending. As AI capex concerns mount, regulatory scrutiny intensifies, and valuation multiples compress, capital is reallocating. Equal-weight indices are outperforming cap-weight. Small-caps are catching bids. Sector dispersion is widening.

This isn't bearish, it's healthy. Markets function best when leadership rotates and breadth expands. The problem is that most portfolios are still overweight the same 10 names that worked for 24 months. That trade is crowded, expensive, and vulnerable.

Investors who recognize this shift early—who lean into quality, diversify away from mega-cap tech, and embrace breadth—will capture alpha as the market reprices concentration risk. Those who chase yesterday's winners into the downdraft will learn an expensive lesson about recency bias.

At Daly AM, we're positioning for exactly this environment: systematic strategies that exploit dispersion, avoid concentration, and adapt dynamically as regimes shift. When everyone else is still fighting the last war, we're already repositioned for the next one.

📅 Forward View: Week of December 15-19, 2025

Key Events:

Tuesday (12/16): Retail Sales (Nov) – Consensus +0.4% MoM. Watch for holiday spending strength.

Wednesday (12/17): FOMC Minutes from December meeting. Dissent details and tariff discussions will matter.

Thursday (12/18): Initial Jobless Claims, Philly Fed Index. Labor market stability vs. manufacturing weakness.

Friday (12/19): Q4 Options Expiration – Expect volatility and position squaring.

Technical Levels:

S&P 500: Support at 6,800 / Resistance at 6,950

10Y Yield: Watching 4.30% as key breakout level—steeper curve ahead if breached

Next week brings the final data before year-end positioning. Expect thin liquidity, headline sensitivity, and continued rotation. If retail sales disappoint or jobless claims spike, the Fed's "we're pausing" narrative gets tested immediately. Conversely, strong consumer data could push yields higher and pressure valuations further.

💬 Final Words

Markets don't care about narratives—they care about prices. This week proved it. The Fed cut rates, AI companies crushed earnings, and tech still got obliterated. Why? Because capital finally recognized that concentration is risk, not safety.

The rotation out of mega-cap tech into value, defensives, and breadth isn't a trade—it's a regime shift. Investors who adapt will thrive. Those who don't will watch their portfolios bleed as the same 10 stocks that carried them for two years become anchors.

At Daly AM, we don't chase. We position. We don't predict. We allocate. And we sure as hell don't pay 2-and-20 for someone to put us in the Magnificent Seven and call it "alpha." Join the waitlist here and see what systematic, data-driven investing looks like when the easy money ends.

Disclosures: This newsletter is for informational purposes only and does not constitute investment advice. Past performance is not indicative of future results. Always conduct your own due diligence or consult with a financial advisor before making investment decisions.